If you’ve followed the news you would have definitely read/heard “Jane Street” and “SEBI” multiple times in the past month. Everyone was talking about whether Jane Street had manipulated the market or not. While I don’t have a direct answer to that, I did take the time out to properly understand what exactly did they do. So here’s a (hopefully) easy-to-understand version of Jane Street’s story.

Jane Street is a US trading firm that makes money (insane amounts) by finding tiny price gaps in global markets and trading in literal milliseconds. They handle trillions in trades globally, just to give you an idea of how big a firm we’re talking about.

It started when Jane Street filed a complaint against Millenium Management. They said that their former employees took a secret algorithm they were involved in developing with them from Jane Street to Millenium. It was an algorithm to identify market opportunities in non-US markets and had made them $1 billion in profits. One of the “non-US markets” they were profiting from was none other than India. The lawyers let it slip during court proceedings that Jane Street traded options in India and it raised a lot of eyebrows including SEBI’s. They took a closer look and that’s how SEBI caught on to what Jane Street was doing.

Let’s start by talking about the F&O (Futures and Options) Market. There’s a high risk involved when you’re dealing with futures and options. You might have heard the stat: 9 out of 10 traders in the Indian F&O market lost money between FY22-FY24 (you can read my story about this here). As the name suggests, there are two sides to it:

- Futures: You fix a price today to buy something on a future date. For example, I strike a deal to buy a stock for ₹500 on 31st July. If the stock is trading below ₹500, i make a loss. If the stock is trading above ₹500, i make a profit. The profit or loss can be calculated by simply calculating the different between 500 and the market price of the stock on 31st July. You fix a price and you have to stick to your end of the bargain.

- Options: For a small premium, you secure the right to buy or sell something at a set price on or before a future date. For example, I pay a premium today to secure the right to buy 100 share of a company at ₹500 each by 31st July. If the stock goes above ₹500, say ₹550, I can use my right and buy the stock at a cheaper price. But if it goes below ₹500, say ₹450, I will just walk away from the deal and lose the small premium I paid. There are 2 parts to the premium as well:

- One is value of the option right now. If in the above example, I sold the stock at ₹550, the value would be 550-500 = ₹50. If the stock was at ₹450, I wouldn’t exercise the option so the value is ₹0.

- The second is time value. Even if the option isn’t valuable today, there’s a chance that its price goes up before expiry. So the longer the time to expiry, the higher the time value because there’s more chance for things to go your way.

If you think a stock will go up, you can buy a call option. Basically you’re betting on the stock rising. By selling that call you’re betting on the opposite. If you think a stock will go down, you can buy a put option. Here you bet on the price of the stock falling.

That’s the theory part of the f&o market relevant to understanding Jane Street’s strategy.

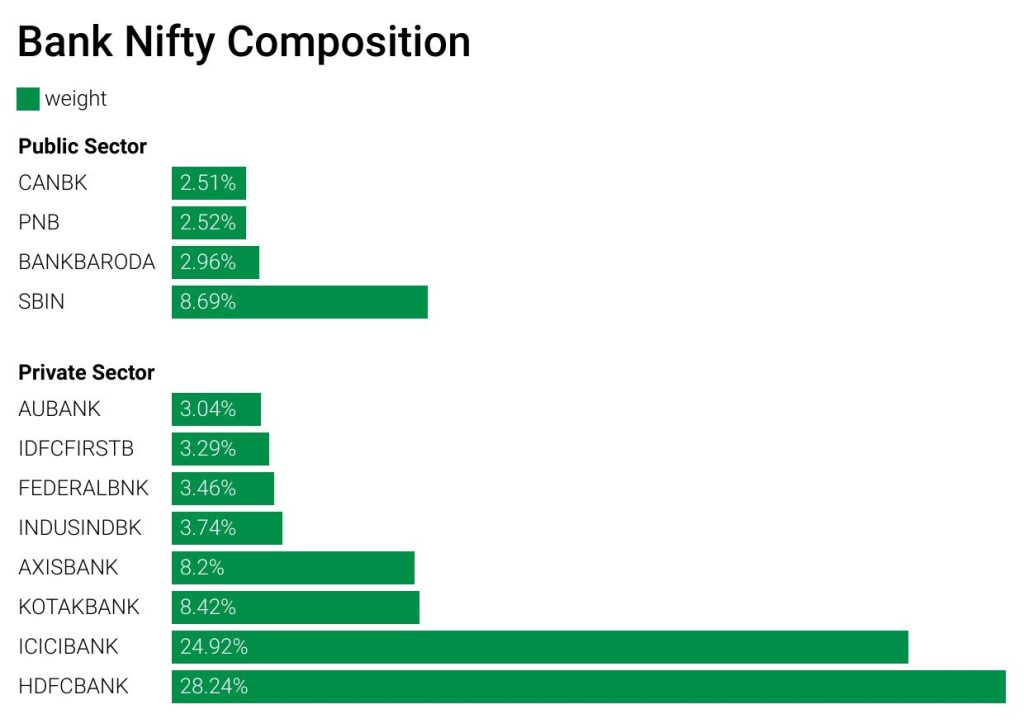

Bank NIFTY is an index that represents the Indian Banking sector’s performance. It includes 12 most liquid and large-cap banking stocks listed on NSE including HDFC Bank, ICICI, Axis Bank, SBI, etc. Even out of these 12 stocks, the top 5 stocks make up 82%.

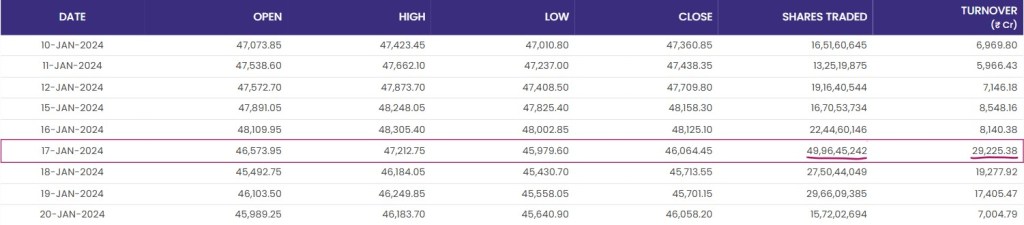

NIFTY has so many indices, why did they specifically choose NIFTY Bank? HDFC is the most liquid of the 12 stocks and the average traded volume is around ₹2,0000 cr per day. Just one set of weekly BANKNIFTY options (the ones expiring on January 17, 2024) saw a jaw-dropping ₹98 lakh crore in notional volume traded in a single day (Jan 16). And here’s the wild part: even the premium paid, which is usually just a small amount to get that kind of exposure, added up to ₹25,000 crore.

Basically, there was way more volume in just the option premium paid than the entire index. And the premiums are only a fraction of the total exposure which means that the volume differential is mind-blowing.

Jane Street’s strategy was simple(ish). They bought shares of big banking stocks that made up the Bank Nifty index. The volume they bought was large, so it pushed up the price of those banking stocks up. Since these stocks are the constitutes of Bank Nifty, it shot up too.

Retail traders saw the index rising and rushed to buy call options, most of them betting on the index rising and the upward rally continuing. These traders just had to pay the premium to buy the call option, which is cheaper than paying the full value of the share in the cash market. As more and more retail traders were buying call options, Jane Street was quietly selling calls to these traders and buying the put option instead.

Once they had gathered enough put options and enough traders stocked up (pun intended) on call options, guess what Jane Street did? They dumped all the bank shares they bought earlier which pushed the price of these stocks and Bank Nifty back down! Now their puts became valuable since the prices were falling. Also, they got to keep the premium from selling call options to the traders because now the call options they’d bought expired worthless.

And that’s how they reported a whopping ₹36,500 of net profit.

Let’s look at 17th January, 2024.

On 16th Jan, HDFC Bank released its earnings after market hours. The market wasn’t thrilled and this led to Nifty Bank opening nearly 3% lower than its previous close.

Jan 17th was an expiry day, which means whatever the closing price of Bank Nifty is that afternoon, determines whether they win or lose money on their options.

When the market was gloomy in the morning, Jane Street bought Bank Nifty stocks and futures. They bought stocks worth ₹4,300 in a falling market! Then they waited till the final stretch before the market closed and aggressively dumped Bank Nifty stocks and futures, dragging the index down right before the final settlement price gets locked in. Since they had already bet on the market falling, they were sitting on a nice pile of cash.

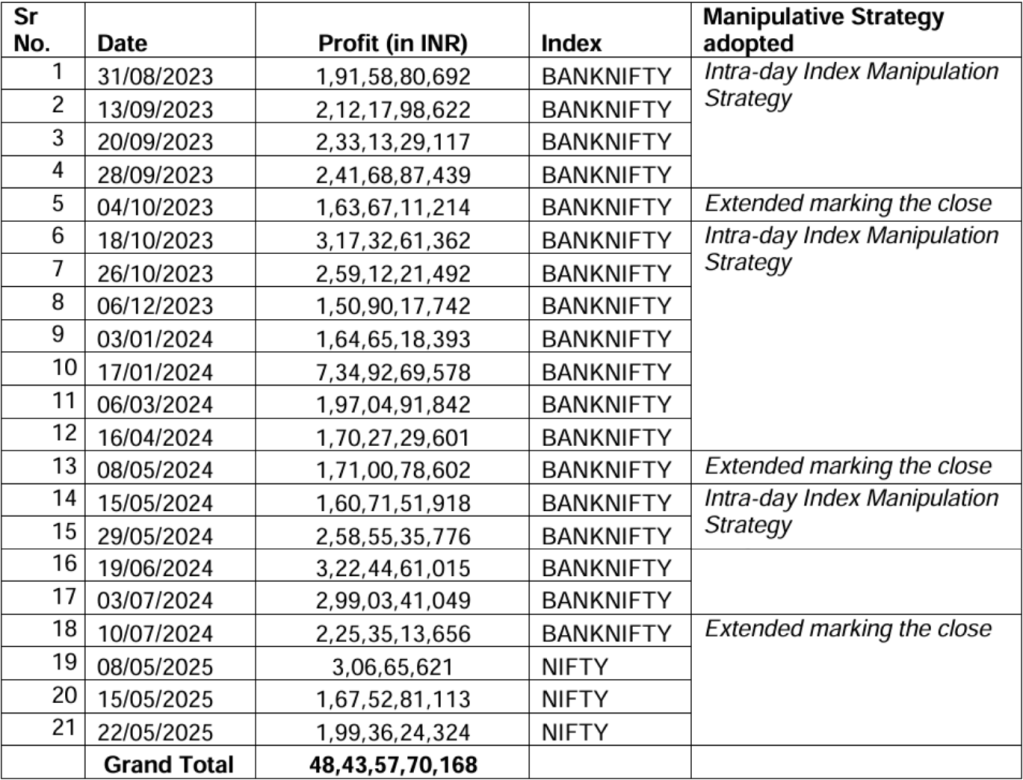

After the court case, SEBI looked at what Jane Street had been up to, purely out of curiosity. When they looked at their profit and loss trail for the period Jan 2023 – March 2025, some eyebrows were raised. They had reported losses as well, but nothing compared to the insane profits they had bagged from Nifty Bank options. They dug deeper and shortlisted 18 days, most of them expiry days, and noticed a pattern like the case of 17/01/2024.

When the sentiment was gloomy, they would buy stocks and futures in the morning pushing the market up. At the same time they would discreetly place bets in the options market that the index would fall later. They kind of orchestrated the Nifty Bank index and options like a puppet master.

It’s actually quite interesting to see the volumes and graphs for the dates that SEBI has identified where “illegal gains” were made by Jane Street. Here are some graphs for January 17th, 2024.

Obviously SEBI was not happy. They placed an interim order on Jane Street. They barred them and all their affiliate companies until the “illegal profits” of ₹4,800 crore can be recovered. In late July, however, SEBI informed Jane Street that their trading ban had been lifted.

But the question remains was it really illegal? SEBI thinks it’s an example of “intraday index manipulation” and Jane Street thinks it’s basic “index arbitrage trading.”

Here’s a full list of the dates SEBI listed out in their report:

You can read SEBI’s Interim Order and the report they published here.

Leave a comment