August bought with it a lot of drama in markets around the world.

To explain what’s going on, first we have to go all the way back to the 1980s in Japan. The economy was doing extremely well against the backdrop of record-low interest rates and soaring stock market valuations. People borrowed a lot of money owing to low interest rates and bought properties hoping they’d appreciated in value. The government soon realised this wasn’t a sustainable model for the economy, so they raised interest rates, causing havoc. You know how the story goes- the stock market crashed and borrowers failed to meet their payment obligations due to high interest rates. Overall sentiment was low and consumer spending decreased so much so that the prices of goods and services dropped to unlivable levels. It was a messy situation. An earthquake, followed by a tsunami, in 2011 didn’t help matters.

Under Prime Minister Shinzō Abe’s “Abenomics” reforms, Japan’s central bank implemented measures to stimulate the economy, including cutting interest rates to zero and printing new money via quantitative easing. This increased money circulation, devaluing the Yen, and made domestic investments less appealing, prompting investors to seek higher returns abroad, further weakening the Yen. These reforms weren’t beneficial for the currency, but the aim was to boost Japan’s economy.

The economic growth never came but the Yen kept losing its value. It was a lose-lose situation.

The yen lost at least one-third of its value against the US dollar between 2021-2024. At the end of April, the currency hit a 34-year low against the dollar, reflecting the shift in its value.

Now you know why Japan’s interest rates are really really low.

Traders are always looking for financial assets to buy and sell. Sitting in front of their Bloomberg Terminal and sipping on a cup of coffee, they came up with the idea of capitalizing on Japan’s low interest rates. It’s more popularly known as Yen Carry Trade, a finance strategy that has gripped investors globally.

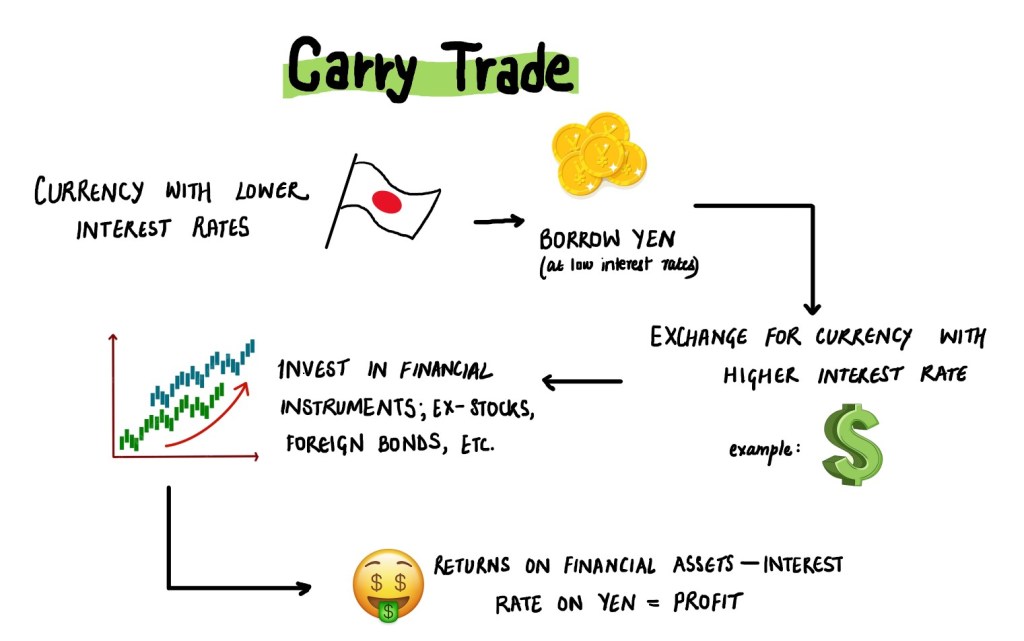

Here’s how it works:

Step 1: Borrow Japanese yen—since the currency is available at low interest rates, it’s an attractive buy.

Step 2: Covert Yen into higher-yielding currency—exchange the yen you borrowed for a currency that has a higher interest rate, such as the US Dollar, Australian Dollar, or any other emerging market currency.

Step 3: Invest in Higher-Yielding Assets—now invest the money you exchanged in higher-yielding financial instruments like foreign bonds, stocks, etc.

Step 4: Profit!!—the difference between the low-interest rate you paid on borrowed Yen and the higher returns earned on the financial assets you invested in makes this trade worthwhile.

Let’s take an example. I borrow JPY at 0.1%, exchange it for INR, and invest in an Indian treasury bond yield offering 7%. Assuming constant currency rates, the investors gains the difference of 6.9%.

Sounds like a good way to make money, where’s the issue?

This is like a real-life game of Jenga with money. Each move builds a tower that’s higher and more impressive, but if one thing goes wrong, the entire tower could come crashing down.

The problem usually arises when the funding currency, in this case Yen, spikes. That’s exactly what happened to the Yen recently. Due to to a cocktail of economic, political, and technical factors, the currency has been pushed upwards, catching the investors off guard. The Bank of Japan began raising rates, especially as there are discussions of rate cuts in the EU and US.

The Yen is strengthening and the carry trade is unwinding.

Seeing the rebound in the yen, investors rushed to dump assets they had purchased by borrowing yen and buying back the Japanese currency to cover their losses. Since this was hardly a hidden trade, other investors also flocked to do the same, pushing the yen up even higher.

Many investors had invested the borrowed yen in equities, so pulling this money out to buy back yen also caused stock prices to fall. The rapid appreciation of the yen compared to other currencies has created volatility in the markets, as evidenced by the rise in the VIX across various markets around the world. Investors are becoming risk-averse and pulling their money out from riskier assets.

There were, of course, other factors at play that explain the major sell-offs we’ve seen in the market over the past week. However, this is definitely one of the contributing factors.

Leave a comment